Posted on May 3, 2023 @ 07:11:00 AM by Paul Meagher

In the last few years, my year end book keeping efforts for our farming venture resulted in a group of text files with each text file dedicated to different expense categories. I also had a text file for income and one for the calculation of taxes collected and paid out. The files were all neat and organized and ready for auditing if it ever came to that. I was audited once and no major issues were found (they generally do have to find something to justify their time). The audit was triggered by a larger than normal tax refund I claimed because I purchased some farm land to add to our farm property and was able to claim most of the sales tax back as we weren't generating much farm income at the time and where I live farm income from hay sales does not require collection of sales tax which was our major source of farm income at the time of the audit.

This year as part of my yearly effort to improve my bookkeeping system I decided to develop a web application called Expense Tracker that would allow me to input and review my expenses online. I developed 4 objects to implement the relevant functionality: ExpenseCategories, Expenses, ExpenseReport, and ExpenseReadWrite (for importing expenses in text file format and viewing them prior to committing them to the bookkeeping database). I refined the Expense Tracker code base in the context of inputing expenses and discovering issues as I went and fixing them. The resulting web application is not something I would release to the general public but it is good enough that I was able to input this years farm expenses into my Expense Tracker and I was able to view a report of my categorized expenses with total cost and total sales tax calculated as well as costs and sales taxes paid out over all categories of expense. I was able to enter category costs directly into my income tax forms.

When I was entering expenses, one feature that became handy this year was an optional "Note" feature for expenses. There are some expenses like Machinery Fuel, Truck Fuel, Electricity, and Internet for example that generate quite a few invoices during the year. Rather then entering each one individually, I found it easier to enter the total cost and total sales tax paid over the year as one expense claim entry. The date of that expense was the billing date of the last invoice for the year. In the "Note" box for that expense I entered a breakdown of all the expenses that I had accumulated into text file and totaled up. This saved me from having to enter all my expenses individually. If I had the time I could have developed some code to import the text file as individual expense entries but the "Note" feature was a big time saver this year and allowed me to complete my taxes without further pressure before the deadline.

If you tell people you created your own bookkeeping software they are likely to inform you of an app or some other software like Excel they use to track their expenses. There are lots of options out there. My experience, however, is that given my background as a web developer it was not that difficult to develop personal expense tracking software so why not develop something that meets my particular expectations? What would make it more difficult is if I was making a commercial product and had to spend alot of time refining the product for different devices, making it secure and making it look nicer.

What are some improvements to my bookkeeping software that I would like to make?

The "business use of home" and "business use of vehicle" categories of expense can be tricky because you are not claiming the full amount of the entered expenses. Because I had to meet a deadline to file my taxes of May 1st, my expense tracker didn't address this issue and I made manual adjustments to correct for this.

When you purchase more expensive items, you can't claim the full cost in the year of purchase but only some percentage depreciation for that year. I do not currently handle depreciated costs and I made manual adjustments to correct for this.

I don't have an income tracker. The income tracker would allow me to enter income by income category and generate a report of the income coming in from different farm ventures: Concerts, Weddings, Camping, Hay Sales, AirBnB, Bike Rentals, and eventually Wine Sales. Concerts may need to be broken down more into Ticket Sales, Merchandise Sales and Food Sales as we like to separately track these categories of income and expenses.

If I have an Expense Tracker and an Income Tracker, theoretically I should be able to create a farm dashboard that reports what my year-to-date totals are for: Total Revenue, Total Expenses, Sales Tax Collected, Sales Tax Paid Out, Profit.

After many years of making a conscious effort to improve my bookkeeping systems, I'm starting to feel a sense of mastery and that next year will not be a long drawn out process to get my books ready for income and sales tax reporting. We have started entering our expenses so far this year into the Expense Tracker and will hopefully be entering expenses on an ongoing basis rather than throwing receipts in a folder because we are too busy to keep track of expenses and waiting until year end to sort it all out.

Posted on April 26, 2022 @ 08:53:00 AM by Paul Meagher

Currency conversion involves exchanging currency in one denomination (e.g., USD) for currency in another denomination (e.g., CAD). Today, if you wanted to exchange US dollars for Canadian dollars, 1 US dollar would yield 1 dollar and 28 cents in Canadian currency. The yield often varies in ways that exhibit a trend. Investors often look for opportunities to exchange currency when the exchange rate appears to be approaching a peak before it goes down again. Currency exchange platforms can be setup to notify you when a certain exchange rate is exceeded which might be your signal to buy the target currency.

The purpose of this blog is not to discuss foreign exchange (forex) trading but to use the idea of currency conversion as a way to think about capital conversion.

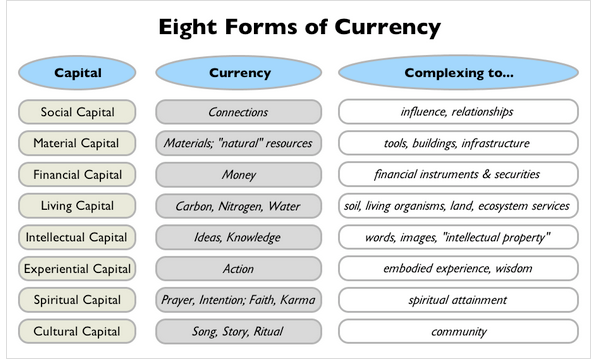

Capital Conversion, as I will use the term, refers to any conversion, or flow, between the 8 forms of capital discussed by Ethan Roland & Gregory Landua in their often cited essay 8 Forms of Capital (2011).

The 8 forms of capital they identified are: social, material, financial, living, intellectual, experiential, spiritual, cultural. The 8 forms of capital appear as 8 forms of currency shown in this essay diagram.

The importance of the concept of capital conversion arises because it can potentially be used as an explanatory framework for how a business might get off the ground and why certain businesses get funded.

A business might get off the ground by converting different forms of capital into financial capital. For example, a person that has an active and positive presence in a community might be able to convert social capital into financial capital if they started the right type of business in that community. The conversion rate may not be high resulting in rapid wealth, but it could be what gets you started and helps you to continue to grow financial capital and other forms of capital over time.

In terms of funding, a startup might be worth funding because they are a store of several different forms of capital (social, material, living, intellectual, experiential, spiritual, cultural) that can be converted to financial capital sufficient to generate a return for an investor.

The main takeaway of this blog might be the idea that starting and funding a business can be understood as a capital conversion process between the multiple forms of capital.

Curtis Stone has a nice video in which he discusses these different forms of capital.

Posted on March 9, 2022 @ 08:15:00 AM by Paul Meagher

In my previous blog I applied the concept of a "payback period" to a farm investment I recently made, namely a portable toilet. In this blog I want to apply the concept to another recent purchase I made, discuss limits to its application, and how it might mislead you into making a bad investment.

Oil Fryer Example

This is the time of year that I like to make investments for our farm property for the year ahead. Our primary focus this year will be hosting on-farm events and hopefully selling our wine (once we get licensed to sell). We anticipate generating at least double the revenue this year from farm events. Some of the investments we need to make in order for that to happen should be made now rather than after revenue is earned from the events. The concept of a "payback period" can useful for determining if certain equipment purchases might be worth investing in or not.

At our last event in 2021, we tested out a 4 gallon oil fryer for making french fries to see if we could offer good quality fries and how people would respond. We had good demand and people enjoyed them. The fryer attaches to a normal propane cylinder and can be operated outside like a barbeque. It fries using 4 gallons of cooking oil which means it doesn't decrease in temperature too much when you dump fries previously soaking in water into it. This means you can potentially keep up a fairly steady rate of fry production however there is some loss in temperature even with 4 gallons of oil. The fryer has two baskets so I try to cycle the baskets so they are not being loaded with fries at the same time and this helps to alleviate that problem and maintains steady production.

We used our last event in 2021 to 1) figure out a process for slicing up the fries efficiently, 2) gauge the rate of production of fries,

3) determine what container we would use and how many fries we would include, 4) what condiments we would offer and 5) what we would

price a serving at. This experiment in selling fries was more about testing systems and learning than it was about making money. One thing I did

learn was that if we wanted to serve fries to +500 people at an event this year, we would need at least one more fryer. Yesterday I decided to pull the plug and invested in a second fryer with a final price tag with tax of around $720.

Some simple math might be used to estimate a payback period. If we sell a generous serving of fries for $10 per serving, then 72 servings of fries

would yield $720 in revenues. Of course we have costs in oil, potatoes, condiments and containers that might mean we have to sell 100 servings

to recoup the investment. Nevertheless, I would expect this $720 investment to be recouped on the first outdoor concert event and then we are into revenue generating territory. The fact that an additional fryer would be required to generate more food revenue from fries, and that the payback period is very short, makes it a good investment for the farm. It should be noted that my decision to buy the first oil fryer was based on a food truck selling out 250 lbs worth of fries during our first event so I knew there was good demand for that type of food offering.

Payback Period Limits

Some equipment purchases seem to be more readily analyzed in terms of payback period than others. Some equipment you just need to purchase and it doesn't necessarily generate an obvious payback. An example is a lawn tractor that we need to purchase this year as our

existing one is starting to breakdown more frequently and we rely upon it quite a bit. Mowing grass helps make the property look nice and is used to maintain the vineyard and orchard but it is hard to put a price tag on that and it is hard to avoid the need for lawn mowing. In contrast, if I were purchasing a mower that would be used to make square bales then I could use the revenue generated from the square bales to compute a payback period. While I think the concept of a payback period is helpful in making decisions about equipment purchases, it does not obviously apply to all equipment purchases

you might need to make to run your business. When the required equipment is not linked to saving or generating money, other factors come into play to determine the particular piece of equipment you might decide to purchase.

Payback Period Failure

I purchased 9 bicycles 4 years back thinking I would rent them from the farm. That business never really took off. As I was purchasing

the bikes I was already counting the money I would be making renting them a few times a week. I got the bikes for a good price. A bike

shop was getting rid of 5 hybrid bikes it was using for rentals and the rental season was over. I later purchased 4 new mountain bikes for a good price on a year-end clearance sale.

One issue that I didn't really anticipate was the space the bikes would take up, especially if you include helmets, repair stand and

extra parts. It almost requires it's own small building. I have been storing them in the barn but they are mostly just taking up space that I would rather use for other purposes. When you take into account the space requirements, and the market cost of storage, the total cost would go up significantly and the payback period would lengthen considerably. So, keep in mind other costs that you might not be considering when you purchase revenue generating equipment, especially the storage aspect.

I also didn't give enough thought to the disadvantages of renting from my farm. The biggest disadvantage is that you have to peddle

2 miles (4 kms) up a fairly steep hill to get to our farm. You have to be a pretty dedicated bicyclist to want to drop off your car at our farm, go downhill for a day riding the countryside, and then finish off your day cycling up a steep hill for 2 miles. For this business to work involves more complex logistics than renting from my farm. I would do better by bringing the bikes to a better location and picking them up from that location. I don't have the time to hang around trying to sell bikes off farm so this didn't happen. The bike rental business is currently a small sideline and I should decide this year if I want to keep doing it or sell my fleet.

My bike rental business was also disrupted last year by a nearby e-bike competitor who dedicated all his time to renting e-bikes and attracted customers who might otherwise have considered renting a traditional bicycle. It is worth giving serious consideration to whether you might not achieve your payback period because your business could be disrupted by other competitors.

Conclusions

Where you can easily apply a payback period to a purchase, and you have some evidence that the equipment will either save costs

or make money, then it can help to guide your decision making towards making a good purchase for your business. The payback

period concept is not useful for some equipment purchases that have no obvious relationship to saving or making money.

Also, you must be careful not to convince yourself that an equipment purchase will have a short payback period by not taking

into account all the factors that should be entering into the decision (e.g.,storage costs, location of your business, availability

of labor, interest rates on a larger purchase, competitors, etc..).

Posted on February 25, 2022 @ 03:53:00 PM by Paul Meagher

In this blog I want to discuss the concept of a "Payback Period" and how it can be used to analyze an investment decision.

I will use a recent investment I made to illustrate the application of the payback period concept.

Early this week I purchased a used Portable Toilet of the type that you use at outdoor events or for construction crews. It was pretty near brand new and I paid $1000 for it.

We held a couple of multiday weekend events last year at our farm that required renting portable toilets. The cost to rent each toilet was $100 ($25 transport, $75 rental). We will be hosting more events on the farm this year. In a non-pandemic year where there are more events happening, and there is significant inflation in the economy, the portable toilet rental company may need to charge more than $100 per unit for the weekend this year which I consider to be a pretty good deal. By having at least one portable toilet that we own and don't have to rent, a conservative estimate might be that we save at least $200 in fees for renting toilets each year in which case the investment will have a payback period of 5 years or less.

The payback period could be faster if we managed the portable toilet unit on site by transferring waste to a larger storage tank and only bringing in a vacumn truck to empty that larger storage tank. Sounds gross but I spent some of my youth shovelling cow manure into a wheel barrow so I am not easily grossed out by the thought of human manure handling.

Purchasing the portable toilet also gives us the ability to offer washroom facilities at the barn without having to make a larger investment into septic system upgrades right now. We can also be flexible in where we setup the portable toilet.

We have our first wedding event planned for the barn this year. We will likely rent the portable toilet out for wedding events which would speed up the payback period and start generating profit once the payback period is reached.

The payback period concept is a useful concept that can be used to think about investments involving buying certain goods that might assist your business. The payback period for an investment can change under different scenarios for how the purchased asset might be managed. Generally there are several different factors that people take into account when making an equipment purchasing decision and if the decision seems like a good one from several different aspects then it might be a good purchase to make.

Posted on March 20, 2020 @ 07:41:00 AM by Paul Meagher

How do you manage your books? Many people use accounting programs like Quicken that offer a broad array of useful accounting functionality. Some people like to use a spreadsheet to manage their books. Me, I generally use a text file to manage my personal, sole proprietorship, and partnership books.

Every year I try to improve my book keeping systems. Last year I tried to get into the habit of using an accounting program for the farm partnership which never really got traction. In part it is because there was quite a bit of learning to setup the company and then I needed to log in regularly to keep the books updated and that just never happened.

This year I thought I would move to using a spreadsheet program and take advantage of some of the calculation and reporting capabilities of the program. My corporate accountant likes to put all the transactions of my corporation into a spreadsheet to model the company and generate reports from this model. This inspired me to think about doing the same for the farming venture.

I got my spreadsheets and categories setup to be able to efficiently enter all my bills and started entering some bills. Not being a regular spreadsheet user I found it cumbersome to do data entry compared to updating a text file. My accountant exports transaction data into his business spreadsheets which is not the same as having to enter each transaction individually into your books. Ultimately, I got hung up on the spreadsheet approach because it seemed like there were extra steps involved in moving dated entries around when you found a dated entry that fit between existing dates. This happens all the time with the sorted monthly lists of paper receipts that I have to enter.

Yesterday it occurred to me that I am going back to my old text file accounting approach because I believe there are still ways to improve upon this basic approach. I thought I would share with you some of my thoughts on how I intend to do so. I am not advocating this particular approach for everyone as everyone has their own skills and preferences. Because I have programming skills and regularly use a powerful text editor (Ultraedit), this approach seems the most natural to me. Also, this approach is for personal, sole proprietorship and a 2 partner business ventures (the farm). For firms with more employees and more volume, it

is likely not feasible.

In a nutshell, what I realized is that if I pay more attention to how I structure my accounting text files that this opens up the possibility of developing programs to read the file and display the contents of those files in organized, editable lists with nice reports. I could potentially have the best of both worlds: easy to update text files of expenses and income and programs I can incrementally develop to read and display them in various ways including adding, deleting and updating entries though a web interface.

Am I recreating the wheel here? Yes, but the job doesn't appear to be that difficult compared to the time I would have to invest in mastering somebody elses software or approach. Opening and parsing through text files is not a big deal when the text file contents adhere to a structure, which they already do, but I realize now it could be better if I want programs to read them. If you are a programmer it is not a big deal to develop a program that reads through structured data and visualizes the data as, say, lists of expenses by category with tax and cost totals for each category of expense.

What about all the nice data entry features that a spreadsheet or accounting program has? Alot of these features are unnecessary for the main task that I have to accomplish which is to fill out a Statement of Farming Activities form with numbers in the various provided slots - how much on was spent on fencing, how much on plants, how much on machinery repair, how much on fuel, how much on small tools, how much on office supplies, how much on legal, etc...

A text file editor like Ultraedit has alot of powerful features that spreadsheet programs and accounting programs do not have. I can, for example, have visually aligned columns of numbers and can use my cursor to create a selection around that column of numbers. I can then select a column function to compute a sum from the selected numbers. I then enter that number below the column as the sales tax or cost total for that expense category. Alot of what you do in a spreadsheet is column processing. Ultraedit also has good column editing features that allow you to select and sum a set of vertically aligned numbers.

Accounting can get pretty complicated and text file accounting might be one approach to manage this complexity. One area where things can get complicated is the Revenue Recognition Model that different accounting standards use. The Revenue Recognition Model for one accounting standard may allow you to mark everything paid as revenue. If that payment is for a contractual obligation over a term then the IRFS standard would require you to only record part of that payment as revenue and allocate parts of the payment to, say, different months of the contract. The argument is that you don't inflate revenues by doing things this way. The redistribution of a payment as earnings over several months is the type of job a programming language is made for. Text file accounting can be a very simple and a very powerful approach to accounting.

Most people who are not accountants do their accounting by creating lists of numbers representing their income and expenses. They might categorize those lists if there are many invoices to deal with. If you want to continue doing your books in this way while making ongoing improvements, then I believe you can do so by keeping these 2 steps in mind:

Step 1) Make sure your lists are entered in a structured way that a computer program might be easily able to read.

Step 2) Use a computer programming language to read these lists and display them. As you gain experience doing this, you may find better ways to structure your lists (i.e., go back to Step 1).

I still hire accountants to review my corporate books but I do my own accounting for my personal, sole proprietorship and partnership businesses (the farm is a partnership with my wife). Every year I devote a blog to how I intend to improving my accounting system and this year it involves Step 1 and Step 2 above. If you are a larger business with multiple employees then I wouldn't recommend this approach but if you are small startup looking to save some dollars by managing your own books then this approach might work for you as well until such time as you have funds to invest in accounting software and expertise.

Posted on September 22, 2018 @ 07:30:00 AM by Paul Meagher

The image of the lean startup is often associated with spending as little as possible to verify your business model. The entrepreneur is living on ramen noodles, making a series of low cost minimal viable products and getting it out in front of potential customers to find out if they are on the right track. Eventually the entrepreneur reaches a moment when they can take on investment because they have reached a proof of concept and now need to scale. This type of business evolution is more likely to happen in the tech world because of the relatively low cost of entry.

Problems arise when we take this startup approach into a nonlean industry. A nonlean industry is one that is heavily regulated and which may require a high level of expenditure before you can even get started. You may need expensive licensing, meet standards that are costly to achieve, buy real estate, build structures, do extensive renovations, etc...

You can't do all these things on a shoestring budget.

Take for example the production of wine. To make a good bottle of wine you can make it with inexpensive plastic pails and glass carboys. To be able to get into the marketplace with your wine is not so easy. There are many regulations and standards that you have to meet before you may do so, even though you may be in possession of a product that a customer would like. In a nonlean industry startups need to raise significant startup capital to deal with regulatory compliance and other costs of doing business before they can even begin to do business. The legal cannabis industry, for example, is a nonlean industry as there are high regulatory compliance costs to doing business in that industry. This is offset by the potentially high reward factor, as it is in any nonlean industry.

Vegetable farming is an example of an industry where you can startup in a relatively lean manner and become even leaner over time. You can start simple but in time your lean operation can become heavily invested in efficiency improving tools and systems like this one:

'

In conclusion, the lean startup movement has a tremendous amount going for it but the image of starting a business on a shoe string budget is not applicable to some industries where other factors (fund raising success, compliance, networking) may have more importance in determining whether you can create a startup in that market.

Posted on September 5, 2017 @ 05:29:00 AM by Paul Meagher

One often cited classic of aglit (agriculture literature) is Maurice Grenville Kains' book Five Acres And Independence first published in 1935

and revised in 1940. The fact that it is still in print and easily purchased is a testament to its ongoing usefulness.

The book consists of 51 short chapters on a variety of critical areas of farm management from growing crops to managing finances. If you can't read the book, reading the table of contents alone (use Amazon's "Look inside" feature) is worthwhile because it is a masterful summary of the books contents.

The book contains lots of diagrams and figures because it is meant to provide practical instruction on a variety of farm matters. Again, if you don't have time to read the book cover to cover, simply browsing some of the diagrams would be a good way to quickly assimilate some useful content. For example, in the days before electric pumps, an hydraulic ram system was a way to use water to pump water. Here he shows how to setup an hydraulic ram system for use in the field:

Or in the home:

If you do have time to read the book, then you can consult the sections that are most relevant to you. The information does not seem too dated and it is useful to hear the perspective of a successful farmer from 80 years ago to see how they solved many of the same problems that farmers face today.

Some of the chapters that I read about first are his chapters on finance, capital, and accounting. In his chapter on Farm Finance I came across the idea of "hiring money". In the quote below, the masculinity of the pronouns dates the writing and the culture of farming that existed then but the points are still valid:

To determine ways to make money in farming the annual budget and the annual inventory are of prime importance. When the farmer starts business and at the beginning of each of his business years (which may be calendar or his own fiscal year, say March 1) he makes his inventory, then estimates his probable gross expenses and income for each month and for each crop or department so as to determine in advance at what time he is likely to be pinched for money, when he will have surplus, when he must borrow and when he can repay. Knowledge of business methods teaches him that hiring money is the same as hiring labor. [Emphasis mine] So he shows both his budget and his inventory to the cashier of his local bank and arranges for loans perhaps months before he will actually need to borrow. ~ p. 57

I think the notion of "hiring" money is an interesting one that potentially allows us to think more clearly about the role of capital than the notion of "borrowing" money. When a business needs money to startup, expand or as working capital that money is not borrowed but rather hired for a specific job that will ideally return an amount greater than the borrowed amount. We hire labor because their labor generates more revenue than it costs. Likewise, we hire money when we see an opportunity to generate more revenue than it costs.

The metaphor of hiring money encourages us to think about treating any money we might require to finance operations in the same way we would treat money used to hire labor. It needs to generate similar returns to be worth hiring. The metaphor of borrowing money is unhelpful in this regards - you are just putting it back into the original storage without any suggestion that it needs to generate a good ROI for the employer of the capital.

One other aspect of the book that intrigues me is the value assigned to "independence" in the title of the book. In these days of social media, I'm not sure you would be successful promoting the virtues of independence, but there was obviously a time when independence was highly valued, perhaps in the same way that resilience is valued today.

Posted on April 24, 2017 @ 01:17:00 PM by Paul Meagher

I am a fan of April Wilkerson's Do-It-Yourself YouTube Channel. She has developed lots of great video content and her channel continues to evolve. Recently, April and her husband sold their house so she does not have a shop to work from. Her husband agreed to share his shop space with her and this video shows them getting the shop organized for their upcoming DIY videos.

This video motivated me to get myself organized to get my taxes done. I am not the best example of how you should manage your taxes as I leave it to the last minute and throw all my receipts into piles that have to be sorted out later. If you find yourself in a similar situation, maybe you will find my method of getting receipts organized useful.

Below is a photo of my office computer and chair. In the middle, is a pile of receipts. The receipt piles come from different times of the year. I have 12 open folders positioned around my office chair, one for each month of 2016. The first level of sorting for me is to simply move all the receipts into the month folders. I do try to keep automotive receipts, gas receipts, construction receipts, small tools, and office receipts somewhat separated inside each folder but don't try to organize them more than that as I'm doing my initial month sorting.

This setup allows me to keep working on my computer and listen to YouTube videos for entertainment as I sort my receipts. Organizing myself by month allows me to more easily compare my receipts against my bank and credit card statements which are also organized by month.

Once I have my receipts organized by month along with printed monthly bank and visa statements, I then go through each folder month by month and assign receipts to expense categories I've developed for my sole proprietorship businesses. When I finish going through all the months I can then tally the totals in all my expense categories for 2016. The rest of my taxes are relatively easy to do once my expense totals for different expense categories are calculated.

I use an accountant to help me with my corporate taxes which are mostly all digital transactions so the organizational process is much different. I do try to improve my book-keeping system a bit every year. Last year I setup separate banking/credit card accounts for each separate business (3 of them) and my personal account. I can do alot more of my accounting work digitally this year so am less reliant on sifting through paper receipts; however, it can still be difficult to reconstruct what you did last year from a simple bank transaction - you often need the paper receipt to figure out what you purchased.

Someone more organized than me would be updating their expense categories on an ongoing or monthly basis. I hoped to do that last year, but it never happened and I'm not doing so hot again this year. I may have to repeat this process again to get caught up for 2017 so I have a better sense of what my expenses are. I know that monthly tracking of expenses is the next improvement I have to make to my accounting system so I have better real-time information about the state of my separate lines of business.

Posted on March 21, 2017 @ 11:41:00 AM by Paul Meagher

I recently came into contact with the phrase Profit Resilience from reading Zach Loeks new book The Permaculture Market Garden: A VISUAL Guide to a Profitable Whole-systems FARM BUSINESS (2017). In the farming industry there is the problem that profits often don't come in steadily throughout the year and this can obviously be challenging for the farm business. To maintain income the farmer may have to take out loans to cover costs until the next production and sales period happens. Or, the farmer might create another line-of-business designed to generate income during these slow seasons so that a constant level of profits is achieved throughout the year. The latter option gets you closer to profit resilience.

Farmers can achieve more profit resilience if they don't rely upon one line-of-business to sustain them all through the year. Profit resilience is

achieved by introducing specific amounts and specific types of diversity into their income stream. I say specific because too much or too little

diversity can be detrimental. If we try to manage too many diverse types of business, then the complexity of managing it all can outweight

the marginal benefit of adding a new line-of-business. One solution might be to make the businesses less diverse so that similar skills can be used to manage each line-of-business (e.g., CSA, specialty crop, Garlic seeds). Unfortunately, the lack of industry diversity means that income may all track the same seasonal pattern we are trying to avoid. To achieve greater profit resilience the diversity of the lines-of-business have to be greater (similar to portfolio investing).

Profit resilience depends upon having the proper amount and types of businesses in your enterprise portfolio. The proper amount is 3 lines-of-business and the proper types are lines-of business whose profits are not correlated in time. Why 3 lines-of-business? This is just to give you a feasible number of businesses to consider in your planning. Ultimately, the number should be chosen based upon looking at all the small enterprises out there that are demonstrating profit resilience and tallying the number of lines-of-business they are engaged in. Ideally we would also examine small enterprises that failed and examine the number of lines of business they were engaged in. If 3 lines-of-business was identified as ideal then this could be a normative suggestion. Why do the lines-of-business we select have to be uncorrelated? This is ultimately an empirical question but, in the case of farming, it is clear that there can be problems with seasonality of income and if you select all your lines-of-business without ensuring the profits from them are uncorrelated or anti-correlated then you may not achieve profit resilience. The Portfolio Theory of investing might also be used to justify the need for a higher level of diversity among the businesses you invest in. The portfolio theory is arguably about achieving profit resilience, and not just profits.

Is the goal of your business to be profitable or to have profit resilience? You can be profitable without having profit resilience. It happens in lots

of businesses. The automotive shop I frequented went under in early February because they hit a low revenue part of their season and were carrying too many overhead expenses (they moved to a nicer shop with higher rents and more staff). Perhaps having more than 1 line-of-business would have helped but maintaining profit levels is made more difficult when you have higher expenses and encounter rough patches.

Everyone has to be concerned about profit resilience even if you are a senior on a fixed income. When you move from the daily grind into retirement it would be nice if you could achieve some profit resilience in the transition. Your income may be lower but if you also lower your expenses significantly you might be able to achieve some profit resilience during this transition. Likewise, if a business is going through a patch of low sales, then cutting out some expenses might help to achieve some profit resilience (difference between revenues and expenses remains relatively constant). You may also voluntarily decide to restructure your business to have lower income but also lower costs. If profit resilience is your goal rather than simply increasing gross revenue then this makes sense to do.

Profit resilience is a temporal concept in the sense that our time to rebound back to a previous level of profitability is measured by some time interval. If your income nosedives and you rebound back to your previous profit level a year later, is that still an example of profit resilience? Probably not. In the business world we tend to measure things in business quarters and that is probably as good an interval as any to use for measuring profit resilience, although monthly accounting is also a very popular accounting time frame.

Profit resilience can be achieved if we plant things today (e.g., apple trees) that might bear fruit in the future. We can't invest too heavily in

the future, however, if we want to retain profit resilience because the future is not generating revenue today. When selecting another line-of-business to add to the enterprises we should have a significant bias towards adding lines-of-business that will generate profits in the near term. One useful example comes from Mark Shepard who purchased more nut tree seedlings that he needed and used the proceeds from selling the extra seedlings to cover his purchase cost and then some. Even though something is being done for the long term it is nice when you can obtain a yield from it in the short term as well.

The term Resilience is popular these days so when I heard the phrase Profit Resilience I thought it was worth spending some time reflecting on various aspects of that phrase might mean. The last observation that I want make about the term Resilience is that it has been contrasted with two other terms - Fragile and Antifragile - by Nicholas Taleb in his important book Antifragile: Things That Gain from Disorder (2012). Profit resilience might be contrasted with profit fragility and profit antifragility, the latter being another concept worth exploring in a future blog.

Posted on July 5, 2016 @ 07:56:00 AM by Paul Meagher

The 2016 Behavioral Economics Guide (PDF) was recently published. The introductory article by Gerd Gigerenzer discussed a research program between his research group and the Bank of England. Some of that research is reported in a paper called Taking Uncertainty Seriously: Simplicity versus Complexity in Financial Regulation (2014). The basic argument being made in these papers is that we would probably do better in regulating banks if we used simple heuristics to decide if a bank was at risk of failing rather that relying upon increasingly complex metrics to arrive at that assessment. Indeed it can be argued that the complexity of the metrics is making it even more difficult to assess the risk of bank failure.

How do we go about deriving these simple heuristics? You can use a framework of multiple fallible indicators to come up with the best set of indicators to determine if a bank might fail or not. Here are some of the indicators they looked at.

Using the indicators that had the most explanatory power, they proposed the following "fast and frugal" decision tree as a basis for evaluating whether a bank is likely to succeed or fail. A fast and frugal decision tree involves making a pass/fail decision at each node so you don't have to traverse all the nodes to potentially make a decision as to the vulnerability of the bank.

The purpose of this blog is to whet your appetite to read some of the linked to papers to read more. It is also to demonstrate an approach to coming up with your own fast and frugal approach for dealing with complex assessment problems (identify indicators, rank order them, and incorporate them into a fast and frugal decision tree or lens model). I'm not aware of this approach having much traction yet among bank regulators and the authors offered up this model as "illustrative" of a suggested approach rather than a real proposed model. That is too bad because such a model would allow the general public to gain a sense of how vulnerable a bank might be to failure. We can't do that with more complex approaches and therein lies one of the the problems with overly complex approaches that don't necessarily perform any better at predicting bank vulnerability that simple approaches.

Posted on March 16, 2016 @ 08:45:00 AM by Paul Meagher

If you have been self-employed for awhile there is a good chance that

will end up owning more than one business entity which you are deriving

an income from or which you are investing money into starting up (and

want to claim those expenses).

I personally have three businesses and resisted the urge to

complicate my banking by setting up a separate bank account and

a separate credit card for each account. It seemed crazy that

I would need 4 banking accounts (which also includes my personal banking account) and 4 credit cards to manage my accounting properly so I resisted setting up a banking account for one of my businesses and getting a credit card for two of my businesses. I convinced myself that all I needed was a "personal" and a "business" credit card. I also convinced myself that I didn't need a bank account for one of my businesses because I was investing money from my other businesses into getting it started and until it was a "real" business I would hold off on setting up accounts.

The fact is that not having all of these banking accounts and credit

cards made my life more complicated because it made it more difficult

to create a proper accounting trail of where money was coming from and

where it was going to. So yesterday I started the process of setting

up a new bank account and two new credit cards. In the future if I decide to setup a new business it will be with the knowledge that I will need

to also setup a banking account for it and a corresponding credit card.

The credit card is not because I'll need the extra credit, it is simply

that purchasing by credit card is often the most convenient way to make

purchase and record it to a specific business entity.

So my advice to anyone setting up a second business is to make sure you setup a new banking account and a new credit card for your new business right away so you can use them to create an easy-to-follow accounting trail for your new business. Don't make the mistake I made and imagine that your banking will get more complicated because you have more accounts and cards; it will actually get easier because the accounting side of your business will get easier and more justifiable.

The rule I now follow is:

1 business entity = 1 bank account + 1 credit card.

One current event that makes the book timely is the US Presidential elections and the race to predict who will be the next US President as well as the outcome of all the skirmishes along the way. A new group of people who will be given credibility in predicting these results will be the people that Philip Tetlock's research program has identified, through testing, as superforecasters. These are people who come from different backgrounds but who share the feature that they are significantly above average in predicting the outcome of world events.

The superforecaster club appears to be an elite group of prediction experts. Philip and Dan analyze what makes them tick in the hopes of helping us all become better at predicting the future. Many of the questions that Philip and Dan ask them are the types of geopolitical questions security intelligence agencies want to have answers to so that they can properly prepare for the future. Much of the research that is reported comes from research sponsored by intelligence agencies. Intelligence involves alot of prediction work so this makes sense.

The second reason why this book is timely is because this is tax time for many people and there is probably no better time of year to figure out a financial forecast for next year. You have your financial performance from last year clear in your mind and your are now 2 months into 2016 and have some current data to integrate into your forecast for 2016. So around now is a good time to exercise your prediction muscle and come up with a 2016 financial forecast. If you don't seriously exercise your prediction muscle don't expect your prediction abilities to get any better.

One prediction that small businesses are required to make each year is their expected income in order to make appropriate quarterly income tax payments. One reason superforecasters are good at predicting the future is because they are good at breaking down complex prediction problems, like yearly financial forecasts, into smaller and easier prediction problems. If asked to evaluate whether Hillary or Trump will win, they don't try to predict the question as it stands. They break it down into all the things that would have to be true in order for the Hillary or Trump presidential outcome to happen and evaluate the likelihood of those component outcomes. Similarly, to come up with a good financial forecast for next year you need to break your prediction down into expense and income buckets and try to estimate how full those different buckets will be.

One business expense that I claim are the books I purchase for educational or blogging purposes. How much will I spend on books in 2016? If I can nail this down fairly well and then nail down how much I'll spend on keeping my vehicle on the road and so on, then I should come up with a better forecast of my expenses for 2016 than if I just used my overall expenses from 2015 as my guide to forecasting my 2016 expenses. One way to improve your tax season experience is to look at it as an opportunity to improve your forecasting skills in a domain where you can get good feedback on your forecasting accuracy. To be become better at forecasting it is not enough to simply make forecasts, you also have to evaluate how well your forecasts did and this is relatively easy in the case of financial forecasting (next year's income taxes will tell you how accurate you were).

So back to forecasting my book expenses for 2016. Superforecasters are good at taking an outside view of the prediction problem before taking an inside view. The outside view is the objective view of the situation. They ask what might be the relevant numbers, statistics, and base rates upon which I can base my forecast. In my case, I can log into Amazon and see how many books I have purchased so far from them in 2016 and use the amount spent so far to project what I'm likely to spend this year. Once I have these numbers than I can take the inside view and ask whether my rate of reading is likely to persist for the rest of the year. As spring and summer approaches, and I spend more time at the farm, I expect my reading to go down. Even though my reading

rate may go down, I nevertheless expect to keep investing at that rate of 1 book a week because my new years resolution was to read a book a week.

So one book a week at an average price of around $30 per book leads me to make an exact prediction of $1,560 (52 weeks x $30 per book) as the expected total for my 2016 book expenses category.

Another feature of superforecasters is that they are not afraid to do a little math. It is hard to assimilate forecast feedback if you don't compare

forecasted and actual numbers. Comparing forecasted and actual numbers is trickier than just comparing two single numbers. It is at

this point, however, that I want to conclude this blog because I think it will take another blog to address the issue of specifying and evaluating forecasts. I also have the second half of the book to read :-)

To conclude, the Superforecaster book is a timely book to read. Financial forecasting is arguably one of the best arenas in which to develop forecasting skill as it involves breaking down a complex prediction problem into simpler prediction problems and the opportunity to gather feedback regarding your forecasting accuracy. Financial forecasting is also a very useful skill so it is a good arena in which to hone forecasting superpowers.

In my next blog on this book/topic I'll address some of the math associated with specifying and evaluating forecasts.

Posted on February 10, 2016 @ 07:25:00 AM by Paul Meagher

Mark Shepard is the author of Restoration Agriculture (2013). He is a no-nonsense ecological farmer and a business mentor to many Permaculture startups. I listened to a

recent podcast featuring him called Permaculture Demand, Starting Up & Organic Valley. This blog was inspired by some of what he had to say.

One topic that Mark Shepard discussed in this podcast is some of his positive experiences as producer number 40 (of 1,800 producers) for the Organic Valley Cooperative.

Organic Valley (OV) is an independent cooperative of organic farmers based in La Farge, Wisconsin, United States near La Crosse, Wisconsin. Founded in 1988, it is the largest organic farmer-owned cooperative in the world with over 1,800 farmer-owners across the United States, Canada, and Australia. Organic Valley markets its products in all 50 states and exports to 25 countries. In 2014, growing annual sales neared $1 billion.

Mark frequently refers to Organic Valley as a "production aggregator" meaning it aggregates production across farmers so that farmers can access larger and more diverse markets. The need for a production aggregator, according to Mark, can arise because there is a failing market for your commodity or service when you are acting alone in the marketplace. If you are at a farmers market with local grower competition and you can't sell your cucumbers or you can't get your price, then the solution may be for cucumber growers to aggregate production and sell the combined product into the same or bigger market that can absorb it at a price that is acceptable. The market feedback you get when you operate alone may be negative but when you cooperate with other producers the market feedback can be strongly positive and encourage you to grow more cucumbers.

If you combine all your cucumbers together and sell them to a grocery chain then you might be paying a fee to a broker who distributes on

your behalf. What if you replace that broker with members of your coop

so that any fees you pay are going back into your production cooperative? The fees might allow you to make more income or receive additional benefits (i.e., pension, dividends, internal jobs) and would help finance the evolution of the production cooperative. Note that this is a different model than Uber, AirBnB and other popular "sharing economy" business models that offers a production aggregator service and collects a brokerage fee but without many additional benefits provided. The alternative to the "sharing economy" business model may be something along the lines of Organic Valley or the very successful John Lewis Partnership in the UK. These companies may not be as "explosive" in their growth as Uber but they are showing high levels of growth and considerable growth potential.

There may be significant costs to setting up a production aggregator (e.g., legal, accounting, software, storage facilities, equipment, transportation, dedicated staff, etc...) and the production aggregator might seek investment to cover these costs. The production aggregator might offer to return investors money (plus interest) over a period of time but could also sweeten the deal with a coop membership that allows the investor to enjoy some of the benefits of the venture. Ideally, the investor's skillset would be useful to the company and an investor might end up paying themselves some of the money invested to carry out the required setup and ongoing work.

Setting up a production aggregator would entail some legal work on the company structure. Often they are setup using a legal trust as the formal business structure but some type of partnership structure might also work and be less legally complex to start out with. I do not pretend to be a lawyer or accountant so don't quote me on any of this.

I'm not necessarily endorsing the view that cooperatives are the end-all and be-all. I'm mostly interested in examining what the motivation for production aggregation might be, how the startup phase of a production aggregation service might be financed, and what types of benefits private investors might receive from their startup investment (i.e., payback with interest, membership benefits, payment for worktime invested).

Also worth considering is what types of objects can a production aggregation business model be applied to that it isn't being applied to today? Examples might be timber production, water production, carbon sequestration and other products or services that might be less tangible.

Posted on January 27, 2016 @ 09:28:00 AM by Paul Meagher

If you are selling your business (or some percentage of it) and you think it is worth $X but your buyer thinks it is worth $X-$diff, then you might still reach an agreement if you agree to the $X-$diff valuation today and the seller agrees to an "earnout" for the remaining $diff if the company performs to a certain standard over an agreed upon time frame. You as the seller get an immediate payoff less than your valuation, but you earn the rest of your valuation if your company performs as well or better than it has in the past.

An earnout seems to be a clever way to potentially reach an agreement between the buyer and seller of a business when there is a valuation disagreement. There are hazards, however, to cutting such deals. Mark Mcleod came out strongly against them arguing that earnouts almost never work

due to alignment issues they can cause between the buyer (who doesn't want to pay the earnout) and seller (who wants the earnout). Mark suggests you treat an earnout provision like a lottery ticket with no strong expections that you will receive it.

Two other issues with earnouts have to do with potential litigation and negative tax consequences. Litigation often arises because there is a dispute as to whether the relevant earnout milestones were achieved and the seller may object that they were blocked in some way from achieving their earnout targets because of the buyers actions. One also has to consider whether the money paid as earnout money is treated the same as the capital gains arising from selling your business or part of

it. Often earnout money is subject to higher taxes. These issues are discussed in more detail in lawyer Roger Royse's article The Problem with Earnouts.

So while earnouts would appear to be a clever bargaining technique in arriving at an agreement between a buyer and seller of a business, there are some negative consequences that all parties should be aware of and make allowances for if they still want to use an earnout to resolve valuation disagreements.

The purpose of this blog was to raise awareness of the concept of an earnout and some of the concerns that cause bloggers and lawyers to often speak poorly of this bargaining technique.

Posted on January 22, 2016 @ 09:02:00 AM by Paul Meagher

In my last blog on the principle of highest use, I wondered whether we might apply the highest use principle to investment capital. The basic idea is that

we would want investment capital to serve its highest use first but also subsequently enjoy other uses that our investment capital might have. The purposes of this blog is simply to explore how we might apply the highest use principle to investment capital. I think it is an idea worth exploring and hope this blog encourages you to come up with your own views on the highest use of capital.

We might begin by listing all the uses of investment capital. When I googled "uses of capital" one result that was helpful was the

Uses of Capital page on the Virginia Capital Partners' website. They list 8 uses for their investment capital. These uses are listed below (visit this page for details on each use):

Growth Capital

Acquisition Capital

Geographic Expansion

Startup Capital

Public Company Assistance

Restructuring

Shareholder Liquidity

Recapitalizations

Management Buyouts

This is a good list of uses for a venture capital firm's investment capital. Many of the businesses that use this website to raise capital seek capital for one or more of these these reasons. Unfortunately it is difficult to order this list and say that one use is higher than the rest. It is also difficult to see how employing capital for one use leaves you with the ability to enjoy other uses for the capital unless you derive a return on your investment that leaves you free to invest in other desired uses. For example, if you invest in helping a company grow, the return from that investment might in turn be sufficient to finance the acquisition of a company or geographical expansion for the company. The highest use principle might suggest the best initial use for your investment capital.

Another way to think about the highest use of capital is to reflect upon your own experiences investing in your business. You definitely want your capital to satisfy as may uses as possible. If you had the choice between purchasing a tractor or a piece of land, what is the highest use of capital? That might be determined by the number of uses I have for the purchased object and whether those uses can return capital that would allow me to re-invest into other uses. The highest use of capital in this case might be a tractor because having the land alone without a machine to work it is not likely to return capital back to me as quickly as having a tractor that can be used for many revenue generating activities and also to develop the land. The revenue generated from using the tractor might allow me to subsequently buy the land and have a tractor to work it which preserves my wealth and potentially allows me to re-invest my capital again. So the highest use principle might help us figure out which of several potential investments is the best use of our capital based on whether one of those investments is more likely to allow us to invest in the other uses for our capital.

Another way to think about the highest use of capital is in terms of maximizing positive impact while preserving wealth. Some call this social impact investing. In this case you look beyond just the monetary returns of you investment to how the investment impacts the lives of workers, the community, and the environment. Henry Ford, for example, said "The highest use of capital is not to make more money, but to make money do more for the betterment of life." Henry Ford may not have

been totally philanthropic when he used his capital to raise workers wages as it lead to his workers being able to afford to buy the cars he was producing. Using capital for "the betterment of life" can feedback and create a virtuous cycle of investing that ensures your money enjoys many uses in other hands before it is finally exported from the community for some commodity that cannot be purchased locally. Ford's capital investments had significant social impact while also preserving his wealth. Some might say the preservation of capital is not required in social impact investing. If not, then we have to ask whether this is the highest use for our capital because once it is used up there may no longer be capital available for other uses.

Anytime we invest money we are concerned with making the best use of our investment capital. The highest use principle encourages us to look beyond the initial use of investment capital to anticipate how the investment might lead to other uses of capital either in your hands or in the hands of others. Ideally you want your investment capital to be preserved so it can be used again for the next best use of capital.

Social impact investing is another way to frame the highest use of capital and the highest use principle might be even more applicable to this form of investing. If you are an investor considering a social impact investment you might want to invest in a project that represents the highest positive use of your capital while also ensuring that your capital will be preserved for the next highest use in the future. Entrepreneurs receiving such funds should realize that the objective of the investor may not be to simply to spend their money on a good cause, but to create enough revenue from their investment to preserve their wealth for the next best use and to create the maximum number of uses in the community where the money is being invested.

Posted on January 8, 2016 @ 10:40:00 AM by Paul Meagher

The price to earnings ratio, or P/E, is a important investment concept.

One reason it is important is because it provides a way to think about how to value the worth of a company. If your company is generating profits then you can use those profits to establish a value for your company. The value of your company is some multiple of those profits. The size of the multiple is the tricky part to figure out.

One factor that determines the size of the multiple is whether you are a private or publicly listed company. The economist Paul

Samuelson calculated that, in a bull market, the multiple for a private company was 3 and a public company was 5. He used gross

revenues as his measure of "earnings" instead of "profits".

Not all revenue streams are created equal. A profit in one industry might be worth more than the same amount of profit in another

industry which would be reflected in higher Price/Earnings ratio in the former industry than the latter. Investors may see more potential for earnings growth in the former industry than the latter.

Yahoo Business publishes an Industry Summary that gives you a rough idea on the P/E for various industries. The "Catalog & Mail Order Houses" industry has an astounding P/E ratio of 955.60 (on Jan 11/2016) which, if you dig deeper, you see mostly reflects the value of Amazon in that industry segment.

The P/E value for different industry segments might tell you something about how to value your revenue stream. Shop around for what might be the best estimate of P/E for your industry. Again, using industry level P/E is only one way to guesstimate what your P/E might be.

My interest in P/E ratios was spurred by reading Marjorie Kelly's analysis of how public companies of the "extractive" type work (see my last blog on Generative Versus Exractive Ownership Design). In particular, I've been studying her systems diagram on some of the main factors influencing profit in a public company and the role that P/E plays.

In this diagram she illustrates how public company Profits can be increased by adjusting the factors in the bottom loop which can be

magnified by the factors in upper loop. If Amazon increases it's profit by 1 million then this gets multiplied by a P/E of 955 which results in a 955 million increase in the valuation of the company. One can see that when Amazon declares a profit it has a bigger effect on company valuation than most companies in the world.

I think it is worth studying Marjorie's diagram for awhile to see if you agree or disagree with her analysis of how Profits in (extractive) public companies are determined - what she calls "the secret of the magic". I also think it is worth studying Marjorie's diagram because it will give you a richer understanding of the P/E ratio by relating it to other economic factors. A definition of the P/E ratio gives you one type of understanding, but seeing how it might work in a systems diagram gives you another type of understanding.

I do want to conclude, however, by pointing out that the P/E ratio is one tool you might use for the purposes of thinking about company valuation.

I'll probably have occasion to blog about the contents of this quirky and wide-ranging book in the future, but today I want to discuss Lars' definition of money which I found interesting:

Money is an information technology that informs us about the value of experiments and rewards those who performed them. ~p. 57

In an earlier section, he elaborates upon this definition as follows:

Money is often described as "a unit of accounting, a store of value, and a medium of exchange", but is also an essential information technology which describes to us the value of a voluntary win-win transaction. Win-win, yes. But win-win how much? The money provides the answer in a simple, common code. Two camels. 20 seashells. One million dollars. Any blabbermouth can fantasize about how much he did for others, but if he does it in a marketplace, we can make a decent estimate of its value by counting the money people gave him for his effort (of course, there are exceptions to that). ~ p. 54.

In perceptual psychology, we might call money a measurement scale where the amount of value in a product or service can be assessed according to the price we assign to it. So when we see that a product has a certain price, we assume it has a certain value. If we don't perceive the product or service as having that actual value then we don't buy it. We might view branding as a way to manage the measurement scale so that the price we assign a product or service has the perceived and experienced value associated with that price.

Ultimately what I like about Lars' definition is that is a definition entrepreneurs might find useful. Money informs us about the value of our experiments and rewards those who perform them.

Posted on October 7, 2015 @ 07:37:00 AM by Paul Meagher

In the begining of the last recession in 2008 when taxpayers bailed out the too-big-to-fail banks, there were some banks that did not suffer similar mortgage default rates as these big banks. These were the

community-owned banks, state-owned banks, credit unions and some other financial institutions with a cooperative, mutual, local, or mission-driven focus.

In her book, Owning Our Future (2013), Margorie Kelly points out that one common feature of these alternative

banks was that they were not profit maximizing entities and had an ownership design that precluded them from simply wanting to generate more mortgage loans so they could maximize profits by selling them off to bigger banks who were creating mortgage-derived securities from them. If the loan went bad for these alternative banks

it often meant they weren't serving their community or their mandate. The care and consideration these banks put into their loans was apparently greater than the first and second tier banks that were geared

towards generating mortgage loans to maximize profits.

Profit maximization, it turns out, may be a good strategy for banks in the short run but it can lead to its own demise when it becomes predatory, impersonal, and purely financially driven. In the long run

banks with an ownership design that represents the community it operates in and which has a mission beyond profit maximization tend to do better. Consider that many of the larger banks probably wouldn't be

around today if they were not bailed out and that many of these alternative banks were not experiencing anywhere near the same level of defaults during the 2008 meltdown.

Ironically, the government fix was to increase the federal deposit insurance requirements, reporting requirements, and auditing requirements for all banks which tended to differentially affect the financial viability of these smaller alternative banks. The regulators apparently did not see, or allow that, the ownership design and

community-based mandate of these alternative banks were the controls that prevented them from experiencing the crisis to the same degree as the profit maximizing banks.

The story behind the crisis is obviously more complex than this but the point of this short blog is to draw attention to the issue of whether banks that are profit maximizing are systemically problematic and whether we can correct this simply through regulatory improvement. Or, does it require an ownership design change coupled with a mandate change to create real systemic changes in banking? Regardless of whether you agree with Margorie's analysis and assessment of the banking crisis, I think Margorie's book (which I also referred to in a previous blog) is useful in helping us to see that there is room for innovation on the issues of who owns a bank and what their mandate is. The design of future banks will hinge fundamentally on these two issues.

Posted on October 20, 2014 @ 04:11:00 PM by Paul Meagher

Mark Dotzour from the Texas A & M Real Estate Centre wrote a blog called

Wall Street Landlords in which he discusses how Wall Street investment firms are buying large numbers of distressed single family homes that are in various stages of foreclosure. Mark published a useful table that lists the investment firms owning the largest number of such single family homes:

What many of these firms are doing with these properties is fixing them up and renting them out for income. Some may sell them when the housing market appreciates again but many of them are happy with the combination of a discounted purchase price and higher than average rental fees so will likely remain landlords for the foreseeable future.

The biggest player by quite a margin is the Blackstone Group, a huge NY-based investment firm with $248 billion in assets under management. The Blackstone Group is leading the way in devising a new financial product, rent-backed securities, based upon the rental income from these properties.

According to Brian Lynch, "Under this business model, the equity present in rental agreements will be aggregated into tranches based on confidence in the financial ability of the tenants pay their rent. The collateralized security instruments from these tranches will have various rates of return based on risk factors from the underlying leases. Should these rent-backed securities default, the security owners may even have an ownership stake in the properties to fall back on". The reason Blackstone is offering these rent-backed securities to investors is to "allow them to free up equity in these properties to purchase even more distressed homes". Investors apparently are quite excited to buy them so other large investment firms in this market are considering similar offerings.

These rent-backed securities setup an obvious positive feedback loop that will lead to Blackstone becoming an even bigger player in the single family home rental market. While institutional investors and pension funds are apparently quite happy to invest in such securities, Occupy Our Homes Atlanta is not so thrilled. They reported that:

Tenants wishing to stay in their homes can face automatic rent increases as much as 20% annually.

Survey participants living in Invitation Homes [Blackstone's brand for single family home rental properties] pay nearly $300 more in rent than the Metro Atlanta median.

45% of survey participants pay more than 30% of their income on rent, by definition making the rent unaffordable.

Tenants face high fees, including a $200 late fee for rental payments.

78% of the surveyed tenants do not have consistent or reliable access to the landlord or property manager.

It will be interesting to see how the rent-backed securities market plays out. Will the relentless profit-maximization of the Blackstone Group lead to ever more complex leveraging of the rental income and home collateral they own (e.g., rental default swaps)? Will blow back from main street put limits on the positive feedback loop that firms offering rent-backed securities can enjoy? Could there be a market failure involving large losses in rental income and investors wanting their money back - or would they end up owning all or part of the distressed homes backing these securities?

I don't have any answers but I expect that the Blackstone Group will be the company to watch in this evolving market for rent-backed securities.

I also wrote this blog in part because I'm interested in learning more about the Blackstone Group holdings in order to understand why they are the largest alternative investment firm in the world. I seem to be running into their name more frequently as a result of the many companies they have acquired or have a controlling interest in.

Posted on September 4, 2014 @ 09:31:00 AM by Paul Meagher

Green Bonds are ways for Governments, Municipalities, Financial Institutions, and Corporations to raise money to support a broad range of green initiatives from erecting wind turbines, to reclaiming brownfield sites, to addressing issues related to climate change, etc... The promise of Green Bonds, like any bond, is that you will get an assured return on your investment after a certain term by providing debt capital to these organizations.

The issuance of Green Bonds has been growing rapidly over the last few years with many financial institutions and

corporations getting into the game at a rapid rate. The

climatebonds.net website keeps a tally of how many green bonds have been issued to date and this year is set to break new records again for the amount of green bonds issued - going from approximately $11 Billion last year to an estimated $40 Billion this year.

One reason why Green Bonds are taking off is because, according to

this economist article,

"55% of pension-fund assets are exposed to climate risks (including heavier regulation of dirty industries); buying green bonds helps offset

such risks". So pension funds want to buy into Green Bonds to hedge against climate risks that other companies in their portfolio might be subject to.

Another reason would include the fact that "US Green Bonds" as issued by the US Treasury are tax-exempt investments

to incentivize investors to buy into them.

Another reason is that corporations see them as a useful way to raise money for certain types of projects. Because green bonds are growing in popularity it is getting easier to raise capital quickly by issuing "Green Bonds" for their green projects.

Finally, many of the projects that these green bonds are being used to finance are simply good investments. Many green energy projects, for example, have relatively low risk with stable long terms returns so why not invest in them.

The story on what green bonds are and how they work is just beginning. Many see a bright future for Green Bonds in helping solve a host of environmental problems. As with anything with the label "Green" attached to it, one must be skeptical of how "green" the projects are that are being funded via "Green Bonds". There is some work to standardize the criteria used for a bond to qualify as "green" but I doubt that everyone will buy into one published set of standards. It is nevertheless worth keeping an eye on how the whole area of Green Bonds evolves in the near term as more governments, large financial organizations, and large corporations throw their hat into the ring by releasing more Green Bonds. It should mean more money to finance green projects in the near term if the rate of release and subscription to these bonds stays at its present level of growth.

Posted on February 11, 2014 @ 02:31:00 PM by Paul Meagher

You have a good idea but need capital to make it happen. You decide to pitch your idea to investors and see if you can find interested investors. You have a good idea and impress some investors who want to

do some follow up with you. They want to know more information about your business. This is where many attempts to raise funds potentially break down. Why? Because some entrepreneurs think fund raising

is all about the idea and haven't invested time into generating some basic financial information investors might want to know as part of their due diligence.

What financial information might that be? Most business plans are expected to include the following financial statements: